Relevance: GS-3: Government policies and interventions for development in various sectors and issues arising out of their design and implementation; Government Budgeting.

Key Phrases: Annual Financial Statement (AFS), Consolidated Fund of India, Contingency Fund of India, Public Account of India, FRBM Act, Demands for Grants, Finance Bill, Money Bill, Revenue and Capital budget, Revenue, fiscal and primary deficit.

Why in News?

- Finance Minister will present the Union Budget 2022-23 on February 1. Let’s look into important terms in relation to the Union Budget.

Keypoints:

The list of Budget documents presented to the Parliament, besides the Finance Minister’s Budget Speech, is given below:

A. Annual Financial Statement (AFS)

- It is provided under Article 112, shows the estimated receipts and expenditure of the Government of India for the upcoming financial year (2022-23) in relation to estimates for 2021-20 as also actual expenditure for the year 2020-21.

- AFS distinguishes the expenditure on revenue account from the expenditure on other accounts, as is mandated in the Constitution of India.

- The Revenue and the Capital sections together, make the Union Budget.

- The receipts and disbursements are shown under three parts in which Government Accounts are kept viz.,

- The Consolidated Fund of India: draws its existence from Art.

266 of the Constitution.

- All revenues received by the Government, loans raised by it, and also receipts from recoveries of loans granted by it, together form the Consolidated Fund of India.

- All expenditure of the Government is incurred from the Consolidated Fund of India and no amount can be drawn from the Consolidated Fund without due authorization from the Parliament.

- The Contingency Fund of India: Art. 267 of the Constitution

authorises its existence, which is an imprest placed at the disposal of the

President of India to facilitate meeting of urgent unforeseen

expenditure by the Government pending authorization from the Parliament.

- Parliamentary approval for such unforeseen expenditure is obtained, expost-facto, and an equivalent amount is drawn from the Consolidated Fund to recoup the Contingency Fund after such ex-post-facto approval.

- The corpus as authorized by Parliament presently stands at 500 crore.

- The Public Account of India: It draws its existence from Article 266

of the Constitution of India. Moneys held by Government in trust are

kept in the Public Account.

- Provident Funds, Small Savings collections, income of Government set apart for expenditure on specific objects such as road development, primary education, other Reserve/Special Funds etc., are examples.

- Public Account funds that do not belong to the Government and have to be finally paid back to the persons and authorities, who deposited them, do not require Parliamentary authorisation for withdrawals.

- The approval of the Parliament is obtained when amounts are withdrawn from the Consolidated Fund and kept in the Public Account for expenditure on specific objects.

- The AFS shows, certain disbursements distinctly, which are charged on

the Consolidated Fund.

- The Constitution of India mandates that such items of expenditure such as emoluments of the President, salaries and allowances of the Chairman and the Deputy Chairman of the Rajya Sabha and the Speaker and the Deputy Speaker of the Lok Sabha, salaries, allowances and pensions of the Judges of the Supreme Court, the Comptroller and Auditor-General of India and the Central Vigilance Commission, interest on and repayment of loans raised by the Government and payments made to satisfy decrees of courts etc., may be charged on the Consolidated Fund of India and are not required to be voted by the Lok Sabha.

B. Demands for Grants (DG):

- Article 113 of the Constitution mandates that the estimates of expenditure from the Consolidated Fund of India included in the Annual Financial Statement and required to be voted by the Lok Sabha, be submitted in the form of Demands for Grants.

- The DGs are presented to the Lok Sabha along with the Annual Financial Statement. Generally, one Demand for Grant is presented in respect of each Ministry or Department.

C. Finance Bill:

- It is presented in fulfilment of the requirement of Article 110 (1)(a) of the Constitution, detailing the imposition, abolition, remission, alteration or regulation of taxes proposed in the Budget.

- It also contains other provisions relating to Budget that could be classified as Money Bill.

- A Finance Bill is a Money Bill as defined in Article 110 of the Constitution.

D. Statements mandated under FRBM Act:

- Macro-Economic Framework Statement: is presented to Parliament

under Section 3 of the FRBM Act and the rules made thereunder.

- It contains an assessment of the growth prospects of the economy along with the statement of specific underlying assumptions.

- It also contains an assessment regarding the GDP growth rate, the domestic economy and the stability of the external sector of the economy, fiscal balance of the Central Government and the external sector balance of the economy.

- Medium-Term Fiscal Policy cum Fiscal Policy Strategy Statement:

It is also presented under Section 3 of the FRBM Act.

- It sets out the three-year rolling targets for six specific fiscal indicators in relation to GDP at market prices, namely (i) Fiscal Deficit, (ii) Revenue Deficit, (iii) Primary Deficit (iv) Tax Revenue (v) Non-tax Revenue and (vi) Central Government Debt.

E. Explanatory Documents:

- Expenditure Budget: Here the estimates made for a scheme/programme are brought together and shown on a net basis on Revenue and Capital basis at one place.

- Receipt Budget: The document provides details of tax and non-tax revenue receipts and capital receipts and explains the estimates. The document also provides a statement on the arrears of tax revenues and non-tax revenues, as mandated under the FRBM Rules, 2004.

- Expenditure Profile: This document was earlier titled Expenditure Budget - Vol-I. It has been recast in line with the decision on Plan-Non Plan merger. It gives an aggregation of various types of expenditure and certain other items across demands.

- Budget at a Glance: This document shows in brief, receipts and disbursements along with broad details of tax revenues and other receipts.

- Memorandum Explaining the Provisions in the Finance Bill: To facilitate understanding of the taxation proposals contained in the finance Bill, the provisions and their implications are explained in this document.

- Output Outcome Monitoring Framework: It will have clearly defined outputs and outcomes for various Central Sector Schemes and Centrally Sponsored Schemes with measurable indicators against them and specific targets for the given Financial Year.

- Key Features of Budget 2022-23: It is a snapshot summary of the economic vision of the Government and the major policy initiatives in the thrust areas of the economy for growth and welfare.

- Implementation of Budget Announcements 2021-2022: The Document summarises the status of implementation of the announcements made by Hon’ble Finance Minister in the Budget Speech 2021-22.

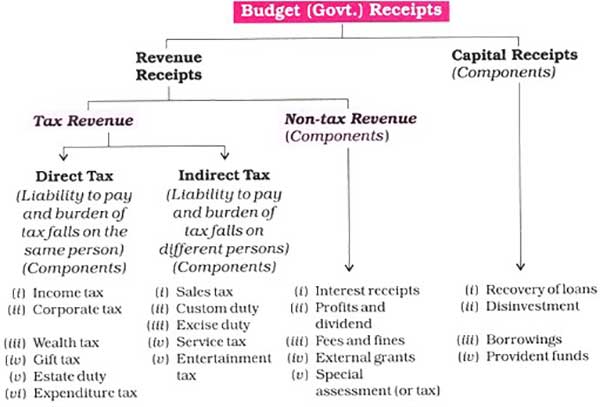

Components of Union Budget:

- The Revenue Budget consists of the revenue receipts of the

Government (Tax revenues and other Non-Tax revenues) and the expenditure

met from these revenues.

- Tax revenues comprise proceeds of taxes and other duties levied by the Union.

- The estimates of revenue receipts shown in the Annual Financial Statement take into account the effect of various taxation proposals made in the Finance Bill.

- Other non-tax receipts of the Government mainly consist of interest and dividend on investments made by the Government, fees and other receipts for services rendered by the Government.

- Revenue expenditure is for the normal running of Government departments and for rendering of various services, making interest payments on debt, meeting subsidies, grants in aid, etc. Broadly, the expenditure which does not result in creation of assets for the Government of India, is treated as revenue expenditure.

- All grants given to the State Governments/Union Territories and other parties are also treated as revenue expenditure even though some of the grants may be used for creation of capital assets.

- Capital receipts and capital payments together constitute the

Capital Budget.

- The capital receipts are loans raised by the Government from the public (these are termed as market loans), borrowings by the Government from the Reserve Bank of India and other parties through the sale of Treasury Bills, the loans received from foreign Governments and bodies, disinvestment receipts and recoveries of loans from State and Union Territory Governments and other parties.

- Capital payments consist of capital expenditure on acquisition of assets like land, buildings, machinery, equipment, as also investments in shares, etc., and loans and advances granted by the Central Government to the State and the Union Territory Governments, Government companies, Corporations and other parties.

Other Key Terms:

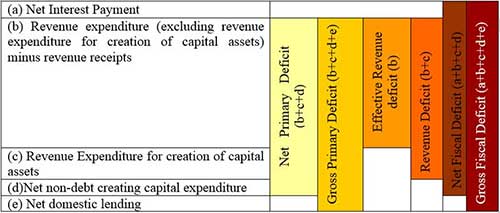

- The excess of Government’s revenue expenditure over revenue receipts constitutes revenue deficit of Government.

- The difference between the total expenditure of Government by way of revenue, capital and loans net of repayments on the one hand and revenue receipts of Government and capital receipts which are not in the nature of borrowing but which accrue to Government on the other, constitutes gross fiscal deficit.

- Gross primary deficit is gross fiscal deficit reduced by the gross interest payments.

- In the Budget documents ‘gross fiscal deficit’ and ‘gross primary deficit’ have been referred to in abbreviated form ‘fiscal deficit’ and ‘primary deficit’, respectively.

- Effective revenue Deficit Introduced in 2011-12, it is defined as revenue deficit minus that revenue expenditure (in the form of grants), which goes into the creation of Capital Assets.

Conclusion:

- The Budget of the Union Government is not merely a statement of receipts and expenditure. Since Independence, it has become a significant statement of government policy. The Budget reflects and shapes, and is, in turn, shaped by the country’s economy.

Source: India Budget

Mains Question:

Q. Explain in brief the various provisions of Government Budgeting in India.