Relevance: GS-3:Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment; Government Budgeting.

Key Phrases: Capital expenditure, Crowding-In and Out, Private & Public Investment, ‘stalling rate’ of projects, debt overhang, Industrial Outlook Survey, Consumer consumption

Why in News?

- In the latest budget, finance minister announced an increase of over 35% in the central government’s capital expenditure to ₹7.5 trillion, amounting to 2.9% of GDP.

Key Points:

- As per the finance minister, “…the virtuous cycle of investment requires public investment to crowd-in private investment. At this stage, private investments seem to require that support to rise to their potential and to the needs of the economy. Public investment must continue to take the lead and pump-prime the private investment and demand in 2022-23.”

- This is quite a shift from the earlier stance of the governments, that

the public investment ‘crowds out’ private investment, the

implicit assumption being that the economy was operating at full

capacity.

- Thus, a rupee more of public investment would lead to a rupee less being available for private investment.

- Further, the only way private investment can rise is if private entrepreneurs ‘offer’ to pay higher interest rates to mobilize funds for investment.

- The implication was that governments needed to cut back on expenditure and borrowing at their end, in order for private investment to flourish.

- In contrast, the crowding-in argument sees public investment as

enabling private investment.

- For example, public investment in road construction in remote areas then leads to entrepreneurs building more factories in such areas, since they are now able to move goods more easily to key markets.

- A 2015 paper by economists at the IMF found that for India, in the post-reform period, public investment does, in fact, ‘crowd-in’ private investment.

- The economy suffered a big hit during the covid period, but is slowly

recovering.

- Analysts across the board have argued that one of the key factors in any recovery will be the willingness of the private sector to invest.

- Despite being a ‘socialist’ economy in the pre-reform era, barring a brief period in the mid-1980s, private fixed investment has consistently been higher than public fixed investment as a share of GDP.

- Starting in the late-1980s, private investment took off, even as public investment actually declined and eventually flatlined.

In that sense, government’s announcement of a big jump in capital expenditure in the public sector, if it does come through, will be a major economic policy shift in the post-reform era.

Issues:

- But the other key feature of this data is the trend since the 2007-08

financial crisis. Private investment peaked at 27.5% of GDP in

that year, and then began a downward trend.

- By March 2020, on the eve of covid, it had fallen to just below 22% of GDP.

- And while public attention is focused on the recovery of the economy

from the disruption caused by the pandemic, the problem of weak private

investment predates the covid era and goes all the way back to the financial

crisis.

- In a sense, the Indian economy has never really recovered from that crisis.

- Even beneath this worrying headline trend, there are a number of

other indicators that point to a serious crisis in private investment.

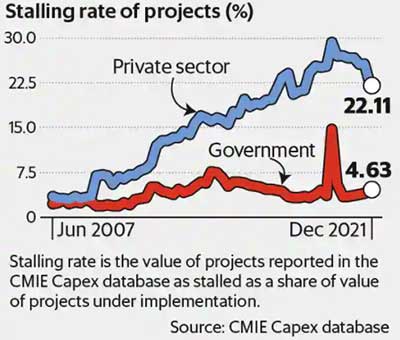

- The Centre for Monitoring the Indian Economy (CMIE) compiles data on capital expenditure, and the status of industrial and infrastructure projects across various sectors and by type of ownership (public sector or private).

- It classifies all projects into different buckets, depending on whether such projects have been completed, are still under implementation or, importantly, have ‘stalled’ for any reason (lack of funds, for example).

- In an analysis of such stalled projects conducted in February 2015,

Economic Survey pointed out that the ‘stalling rate’ of

projects—defined as the value of projects reported stalled as a share of

value of projects under implementation—had risen sharply since the financial

crisis.

- It then also noted, hopefully, that: “The good news is that the rate of stalling seems to have plateaued in the last three quarters.”

- However, the stalling rate has only increased. The bulk of the increase

in the overall stalling rate is due to the stalling of private sector

projects (Chart 2).

- A study done by the central bank of private sector investment last year, based on the CMIE data, reported that the time taken to complete a project, or even to reach a point where it is reported as stalled or abandoned, has increased since the financial crisis.

- One sector that has had a major impact on the stalling of projects is

the power sector, where most private sector projects are, in fact,

public-private partnerships.

- It is facing the persistent problems for over a decade, including fuel supply and regulatory clearances.

- High stalling rates are also seen in manufacturing, though the rate has plateaued in recent years.

Causes:

- Economic Survey’15 attributed different reasons to the stalling of

projects in the private sector versus the public sector: “exuberance”

and a credit bubble in the former, and “policy paralysis” in the

latter.

- It said, first, manufacturing is being stifled by a general deterioration in the macroeconomic environment.

- Second, stalled projects in electricity are a victim of lack of coal (or coal linkages).

- The Indian corporate sector had piled up a large volume of debt in the pre-crisis years to fuel growth.

- This ‘debt overhang’ crisis in corporate India persisted well

beyond the immediate financial crisis that firms faced in 2007-08.

- The slow process of unwinding that leverage has continued to impact the willingness of Indian companies to invest in new projects.

- The share of new projects in the CMIE database as a share of total projects under implementation has fallen from over 10% at the beginning of the previous decade, to around 2% currently.

- On the other side, banks who lent money during the credit bubble, ran up

high levels of non-performing assets as borrowers did not pay their dues.

- It would take a period of time before banks could clean up their balance sheets and be ready to lend again.

Areas of hope:

- Interest coverage ratios (the extent to which gross earnings cover

interest payments) have risen in recent years across public limited

companies, indicating an improvement in balance sheet health.

- Having ‘cleaned’ up their balance sheets, companies could be in a position to invest in new projects.

- As covid restrictions go, and commerce and markets return to normal,

results of the latest Industrial Outlook Survey by the RBI shows a clear

uptick in business sentiment and expectations, going forward.

- The central bank conducts this survey across a sample of over a thousand companies, asking managers their assessment of the current business outlook and their expectations going forward.

- The Business Expectations Index, maintained by RBI, while having dipped slightly in the last quarter is still well above levels of the last several years.

Simply saying, Corporate India seems more optimistic than it has ever been.

Concerns Ahead:

- An improvement in corporate balance sheets, and in business sentiment,

going forward, are only one side of the coin.

- There seems to be a stark divergence between consumer sentiment and business sentiment.Businesses are upbeat about the future, but consumers are not.

- An RBI index of consumer confidence (as opposed to business confidence) is subdued at best.

- Consumers are downbeat about the present—the so-called ‘Current Situation Index’ is still well below pre-covid levels.

- The proportion of consumers expecting to spend more on non-essential items one year ahead is less than half of what it was pre-pandemic.

- Reflecting this, the bulk of business executives in the Industrial

Outlook Survey also expect existing production capacity to be enough to

meet demand, going forward.

- Very few businesses see current capacity as being inadequate to service foreseeable demand.

- Given the weakness in consumer sentiment, it is still an open question whether businesses, despite their new found optimism, will step in to fill the gap.

- This is where public investment could step in, and a 35% jump in

capital expenditure by the government should be welcome. However, there

is less to this increase than meets the eye.

- As CRISIL pointed out in a research note following the budget, accounting for capital expenditure not just in the Central government budget, but also that done by public sector enterprises, the actual increase is less than the headline number.

- This is because a part of capital spending done by public sector enterprises is now being done directly by the Central government, to address the problem of poor execution by public sector firms.

- Further, another component of total public capex is the grants by the Centre to the states for their investments.

- Putting these together, the overall capital expenditure budgeted for 2022-23 is around 6% of GDP, comparable to levels seen before the pandemic (5.9% in 2018-19 and 5.8% in 2019-20).

- More broadly, argues CRISIL, the missing link is the boost to

consumption in the short term—a step that could speed up recovery.

- It says: “This budget has thrown all its weight behind government-led capex in the hope of setting off a virtuous investment cycle to lift growth. What it misses though, is the bridge—short term, consumption-raising measures to address the unequal recovery so far, tilted against large sections of the population particularly in the informal sector, still under pandemic-led duress.”

- Indeed, allocations to schemes that have a direct impact on consumption, such as the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS), have actually seen a dip in allocations for the next fiscal year.

- On the positive side though, allocations to capital expenditure on roads and railways has increased.

- Moreover, a major component of government capital expenditure is done by

the states from grants made by the Centre.

- In the past, state-level capital expenditure has often fallen short of budgeted targets.

Conclusion:

- Ultimately, an overall economic recovery will be heavily driven by private sector investment. Given the weak consumer sentiment, the only impetus can come from government spending, whether to boost consumption (through schemes such as MGNREGS) or investment.

- The consequences of such a decision will become clear in the coming months.

Source: Live Mint

Mains Question:

Q. Capital expenditure by government is a step to boost the economic revival, however it needs to be complemented by private sector investment and consumer consumption. Comment.