Brain-booster /

06 Mar 2022

Brain Booster for UPSC & State PCS Examination (Topic: Crypto Puzzle)

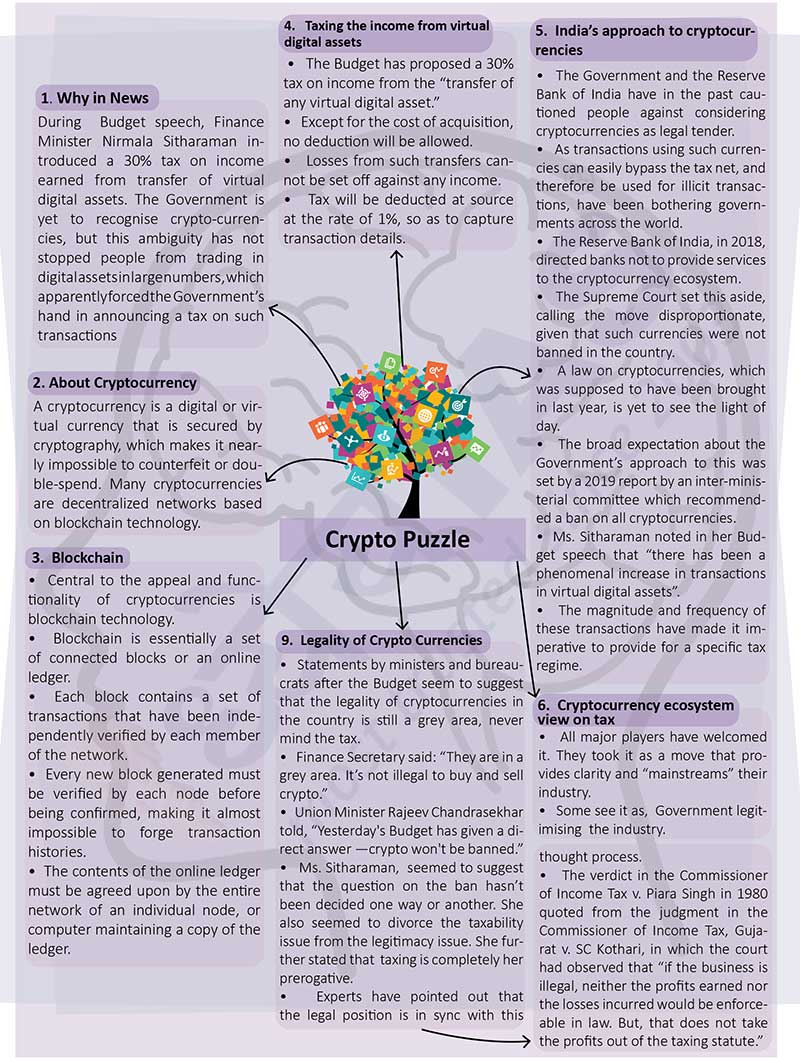

Why in News?

- During Budget speech, Finance Minister Nirmala Sitharaman introduced a

30% tax on income earned from transfer of virtual digital assets. The

Government is yet to recognise crypto-currencies, but this ambiguity has not

stopped people from trading in digital assets in large numbers, which

apparently forced the Government’s hand in announcing a tax on such

transactions.

About Cryptocurrency

- A cryptocurrency is a digital or virtual currency that is secured by

cryptography, which makes it nearly impossible to counterfeit or

double-spend. Many cryptocurrencies are decentralized networks based on

blockchain technology.

Blockchain

- Central to the appeal and functionality of cryptocurrencies is

blockchain technology.

- Blockchain is essentially a set of connected blocks or an online ledger.

- Each block contains a set of transactions that have been independently

verified by each member of the network.

- Every new block generated must be verified by each node before being

confirmed, making it almost impossible to forge transaction histories.

- The contents of the online ledger must be agreed upon by the entire

network of an individual node, or computer maintaining a copy of the ledger.

Taxing the income from virtual digital assets

- The Budget has proposed a 30% tax on income from the “transfer of any

virtual digital asset.”

- Except for the cost of acquisition, no deduction will be allowed.

- Losses from such transfers cannot be set off against any income.

- Tax will be deducted at source at the rate of 1%, so as to capture

transaction details.

India’s approach to cryptocurrencies

- The Government and the Reserve Bank of India have in the past cautioned

people against considering cryptocurrencies as legal tender.

- As transactions using such currencies can easily bypass the tax net, and

therefore be used for illicit transactions, have been bothering governments

across the world.

- The Reserve Bank of India, in 2018, directed banks not to provide

services to the cryptocurrency ecosystem.

- The Supreme Court set this aside, calling the move disproportionate,

given that such currencies were not banned in the country.

- A law on cryptocurrencies, which was supposed to have been brought in

last year, is yet to see the light of day.

- The broad expectation about the Government’s approach to this was set by

a 2019 report by an inter-ministerial committee which recommended a ban on

all cryptocurrencies.

- Ms. Sitharaman noted in her Budget speech that “there has been a

phenomenal increase in transactions in virtual digital assets”.

- The magnitude and frequency of these transactions have made it

imperative to provide for a specific tax regime.

Cryptocurrency ecosystem view on tax

- All major players have welcomed it. They took it as a move that provides

clarity and “mainstreams” their industry.

- Some see it as, Government legitimising the industry.

Legality of Crypto Currencies

- Statements by ministers and bureau-crats after the Budget seem to

suggest that the legality of cryptocurrencies in the country is still a grey

area, never mind the tax.

- Finance Secretary said: “They are in a grey area. It’s not illegal to

buy and sell crypto.”

- Union Minister Rajeev Chandrasekhar told, “Yesterday's Budget has given

a direct answer —crypto won't be banned.”

- Ms. Sitharaman, seemed to suggest that the question on the ban hasn’t

been decided one way or another. She also seemed to divorce the taxability

issue from the legitimacy issue. She further stated that taxing is

completely her prerogative.

- Experts have pointed out that the legal position is in sync with this

thought process.

- The verdict in the Commissioner of Income Tax v. Piara Singh in 1980

quoted from the judgment in the Commissioner of Income Tax, Gujarat v. SC

Kothari, in which the court had observed that “if the business is illegal,

neither the profits earned nor the losses incurred would be enforceable in

law. But, that does not take the profits out of the taxing statute.”